-

采用量子力学中的费曼路径积分方法, 推导出了更符合市场一般化情形的随机波动率股指期权定价模型. 在此基础上, 以恒指期权为例进行实证研究预测30天的期权价格, 同时将Heston模型作为对照组, 并进行稳健性检验. 研究结果表明, 本文构建的股指期权定价模型通过求解费曼定价核的数值解, 进而在线性算法上直接实现股指期权价格的预测, 相比于Heston模型利用特征函数的方法, 不论是在相同到期日不同执行价格下还是在相同执行价格不同到期日下, 定价精度显著提高. 费曼路径积分作为量子金融的主要方法, 本文的研究将为其进一步应用于金融衍生品定价提供参考.

Under the background that stock index options urgently need launching in China, the research on stock option pricing model has important theoretical and practical significance. In the traditional B-S-M model it is assumed that the volatility remains unchanged, which differs tremendously from the market’s reality. When the market fluctuates drastically, it is difficult to realize the risk management function of stock index options. Although in the Heston model, as one of the traditional stochastic volatility option pricing models, the correlation risk between the volatility and underlying price is taken into consideration, its pricing accuracy is still to be improved. From the quantum finance perspective, in this paper we use the Feynman path integral method to explore a more practical stock index option pricing model. In this paper, we construct a Feynman path integral pricing model of stock index options with stochastic volatility by taking Hang Seng index option as the research object and Heston model as the control group. It is found that the Feynman path integral pricing model is significantly superior to the Heston model either at different strike prices on the same expiration date or at different expiration dates for the same strike price. The stock index option pricing model constructed in this paper can give the numerical solution of Feynman's pricing kernel, and directly realizes the forecast of stock index option price. The pricing accuracy is significantly improved compared with the pricing accuracy given by the Heston model through using the characteristic function method. The remarkable advantages of Feynman path integral stock index option pricing model are as follows. Firstly, the path integral has advantages in solving multivariate problems: the Feynman pricing kernel represents all the information about pricing and can be easily expanded from one-dimensional to multidimensional case, so the change of closing price of stock index and volatility of underlying index can be taken into account simultaneously. Secondly, based on the relationship between the Feynman path generation principle and the law of large number, the mean values of pricing kernel obtained by MATLAB not only optimizes the calculation process, but also significantly improves the pricing accuracy. Feynman path integral is the main method in quantum finance, and the research in this paper will provide reference for its further application in the pricing of financial derivatives. -

Keywords:

- Feynman path integral /

- mean pricing kernel /

- stochastic volatility /

- stock index options pricing

[1] Pan J 2002 J. Financ. Ecno. 63 3

Google Scholar

Google Scholar

[2] Eraker B, Johannes M, Polson N 2003 J. Financ. 58 1269

Google Scholar

[3] Broadie M, Chernov M, Johannes M 2007 J. Financ. 62 1453

Google Scholar

[4] 杨智元, 陈浪南 2001 经济研究 47 61

Yang Z Y, Chen L N 2001 J. Econ. Res. 47 61

[5] Duan J C, Zhang H 2001 J. Bank Financ. 25 1989

Google Scholar

[6] 魏洁, 韩立岩 2016 数理统计与管理 33 550

Wei J, Han L Y 2016 J. Appl. Stat. Manag. 33 550

[7] 杨兴林, 王鹏 2018 数理统计与管理 37 162

Yang X L, Wang P 2018 J. Appl. Stat. Manag. 37 162

[8] Bailey W, Stulz R M 1989 J. Financ. Quant. Anal. 24 1

Google Scholar

[9] 谭朵朵 2008 统计与信息论坛 23 40

Google Scholar

Tan D D 2008 Stat. Inform. Forum 23 40

Google Scholar

[10] 韩立岩, 叶浩, 李伟 2012 中国管理科学 20 23

Han L Y, Ye H, Li W 2012 Chinese J. Manag. Sci. 20 23

[11] 樊鹏英, 陈敏 2014 价格理论与实践 34 96

Fan P Y, Chen M 2014 Price Theor. Pract. 34 96

[12] [13] Baaquie B E 1997 J. Phys. I 7 1733

[14] Linetsky V 1998 Computaitonal Ecomomics 11 129

Google Scholar

[15] Baaquie B E, Coriano C, Srikant M 2002 Quant. Financ. 15 333

[16] Baaquie B E 2004 Quantum Finance (Singapore: Cambridge University Press) pp78–116

[17] Baaquie B E, Corianò C, Srikant M 2004 Phys. A 334 531

Google Scholar

[18] Baaquie B E 2013 Comput. Math. Appl. 65 1665

Google Scholar

[19] Rosa-Clot M, Taddei S 1999 Quant. Financ. 5 123

[20] Kakushadze Z 2015 Quant. Financ. 15 1759

Google Scholar

[21] Issaka A, Sengupta I 2017 J. Appl. Math. Comput. 54 159

Google Scholar

[22] Ma C, Ma Q, Yao H, Hou T 2018 Phys. A 494 87

Google Scholar

[23] Paolinelli G, Arioli G 2018 Phys. A 517 499

[24] 陈泽乾 2003 数学物理学报 23 115

Google Scholar

Chen Z Q 2003 Acta Math. Sci. 23 115

Google Scholar

[25] 陈黎明, 邱菀华 2007 中国管理科学 15 12

Google Scholar

Chen L M, Qiu W H 2007 Chinese J. Manag. Sci. 15 12

Google Scholar

[26] 王鹏, 魏宇 2014 管理科学学报 17 40

Wang P, Wei Y 2014 J. Manag. Sci. China 17 40

[27] Heston S L 1993 Rev. Financ. Stud. 6 327

Google Scholar

[28] Scott L O 1987 J. Financ. Quant. Anal. 22 419

Google Scholar

[29] Merville L J, Pieptea D R 1989 J. Financ. Econ. 24 193

Google Scholar

[30] Stein E M, Stein J C 1991 Rev. Financ. Stud. 4 727

Google Scholar

[31] Cox J, Ingersoll J, Ross S 1985 Econometrica 53 385

Google Scholar

[32] 施里夫 S 著(陈启宏, 陈迪华 译) 2008 金融随机分析(上海: 上海财经大学出版社)第192—193页

Shreve S (translated by Chen Q H, Chen D H) 2008 Stochastic Calculus for Finance (Vol. 2) (Shanghai: Shanghai University of Finance and Economics Press) pp192–193 (in Chinese)

[33] 杨爱军, 蒋学军, 林金官, 刘晓星 2016 数理统计与管理 35 817

Google Scholar

Yang A J, Jiang X J, Lin J G, Liu X X 2016 J. Appl. Stat. Manag. 35 817

Google Scholar

[34] Durrett R 2016 Essentials of Stochastic Processes (New York: Springer) pp223–250

[35] Baaquie B E, Kwek L C, Srikant M 2000 arXiv: 0008327v1 [cond-mat] https://arxiv.org/abs/cond-mat/0008327 [2019-5-1]

-

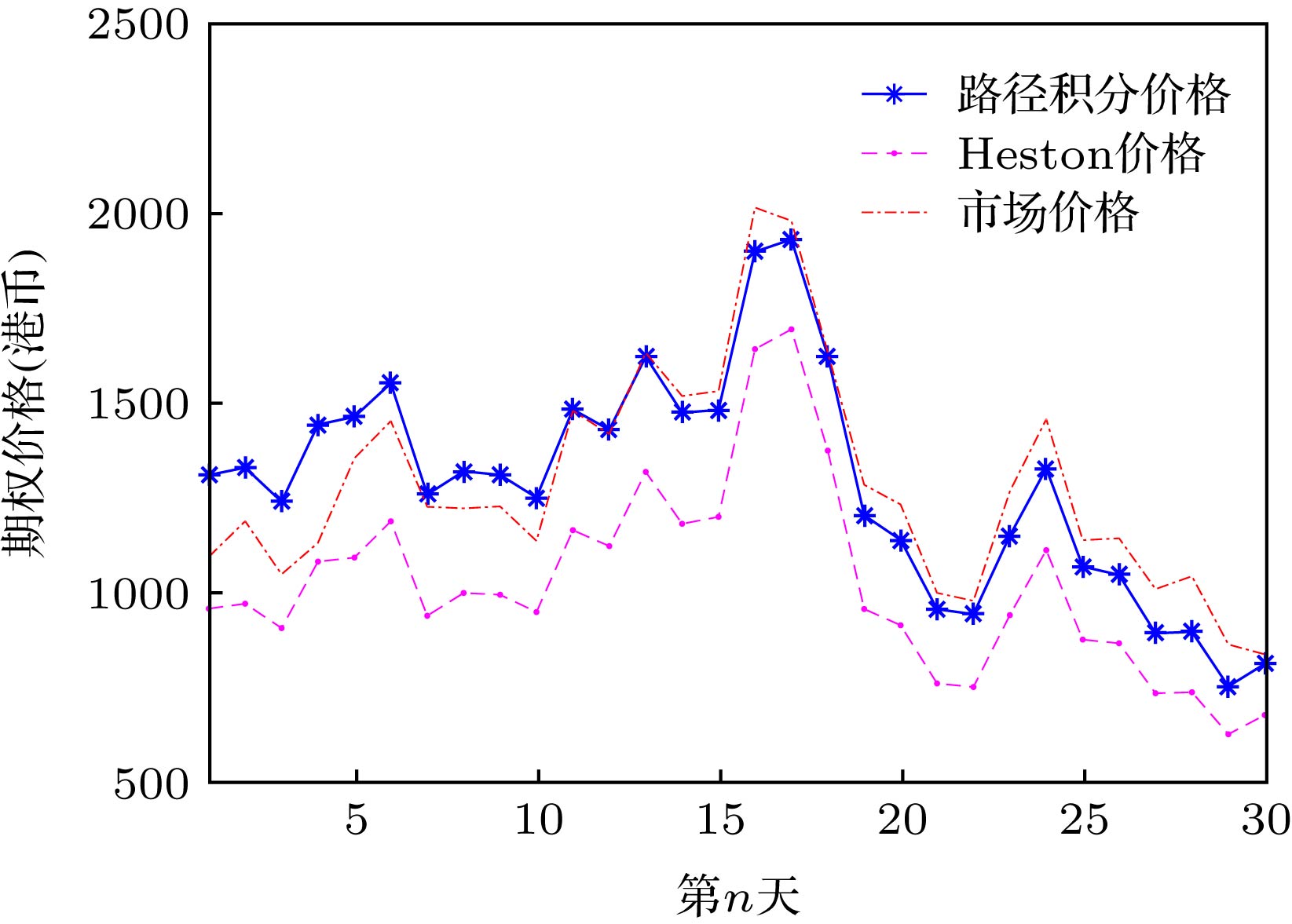

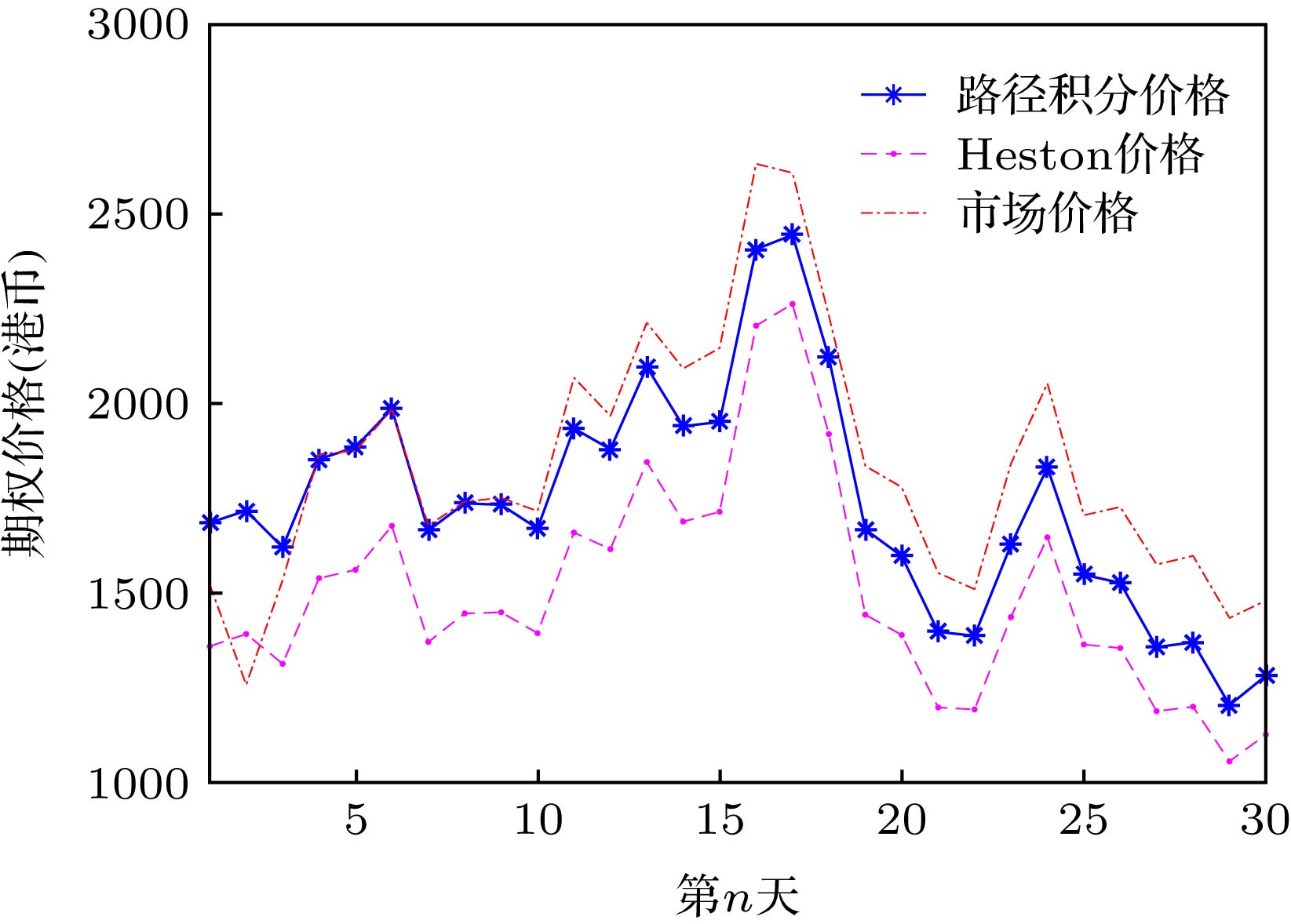

图 7 到期日为2019年2月时两模型的平值期权价格对比图

Fig. 7. A comparison of the two models with maturity date of February 2019

图 9 到期日为2019年6月时两模型的平值期权价格对比图

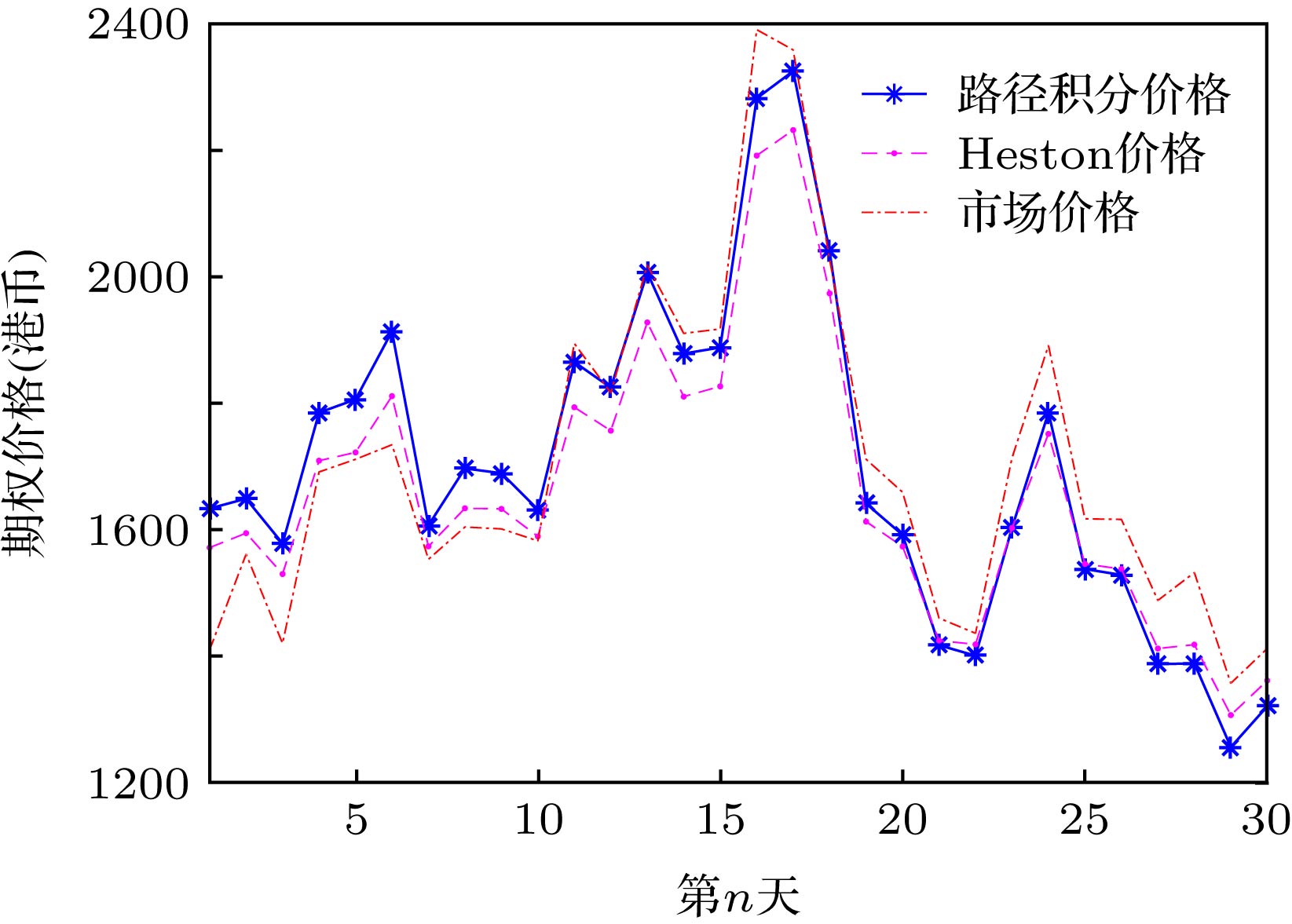

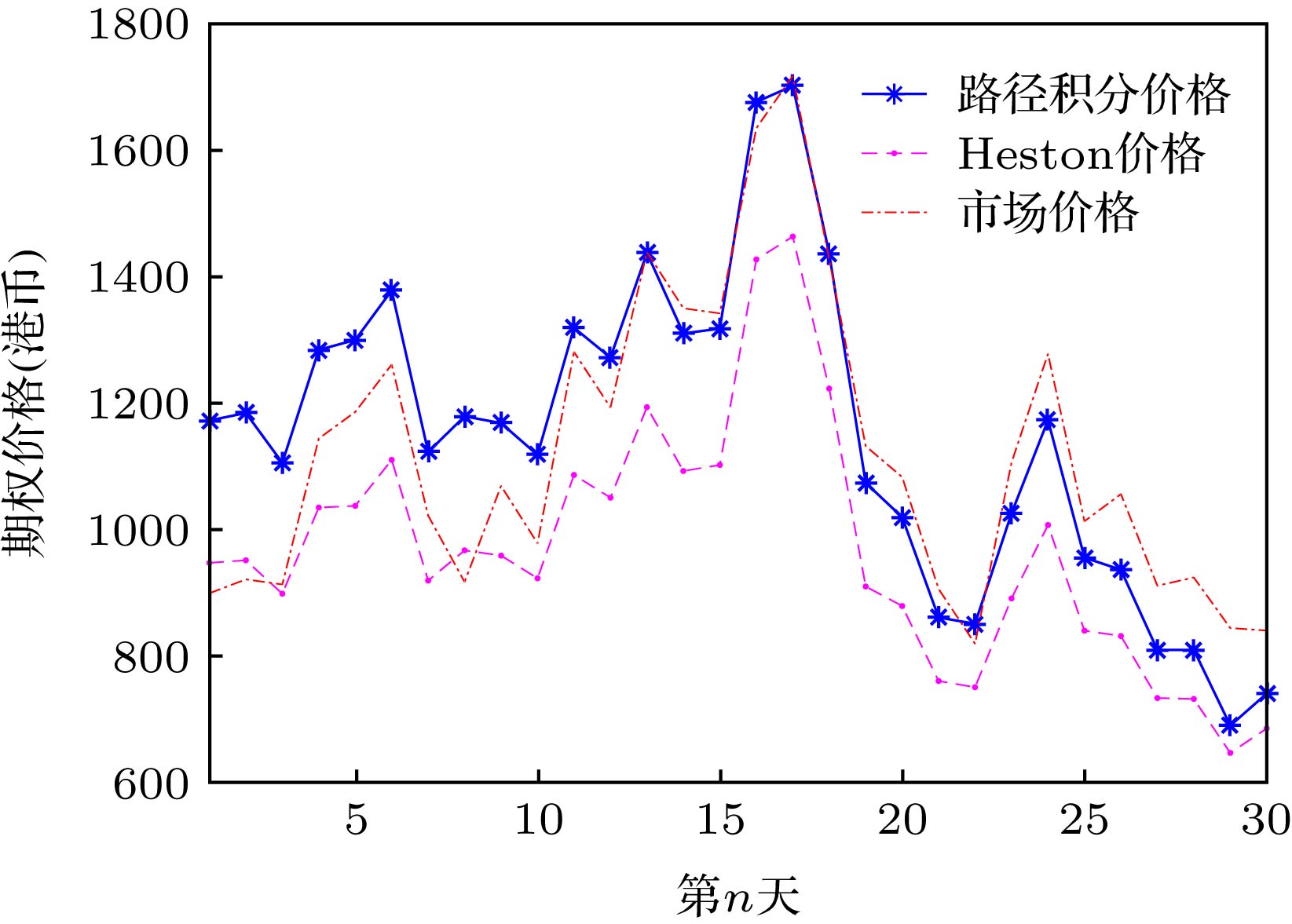

Fig. 9. A comparison of the two models with maturity date of June 2019

图 8 到期日为2019年9月时两模型的平值期权价格对比图

Fig. 8. A comparison of the two models with maturity date of September 2019.

图 11 相同到期日不同执行价格下两种模型的Theil不等系数对比图

Fig. 11. Theil inequality coefficients for the two models on the same maturity date.

表 1 参数估计结果

Table 1. Parameter estimates.

Node Mean sd MC error Quantile Start Sample 2.50% 50% 97.50% α 3.393 0.1539 0.001499 3.082 3.395 3.685 4001 192000 ρ 0.4201 0.2032 0.007068 0.09408 0.4011 0.8774 4001 192000 ξ 1.574 0.07977 8.65 × 10–4 1.416 1.574 1.73 4001 192000  下载: 导出CSV

下载: 导出CSV

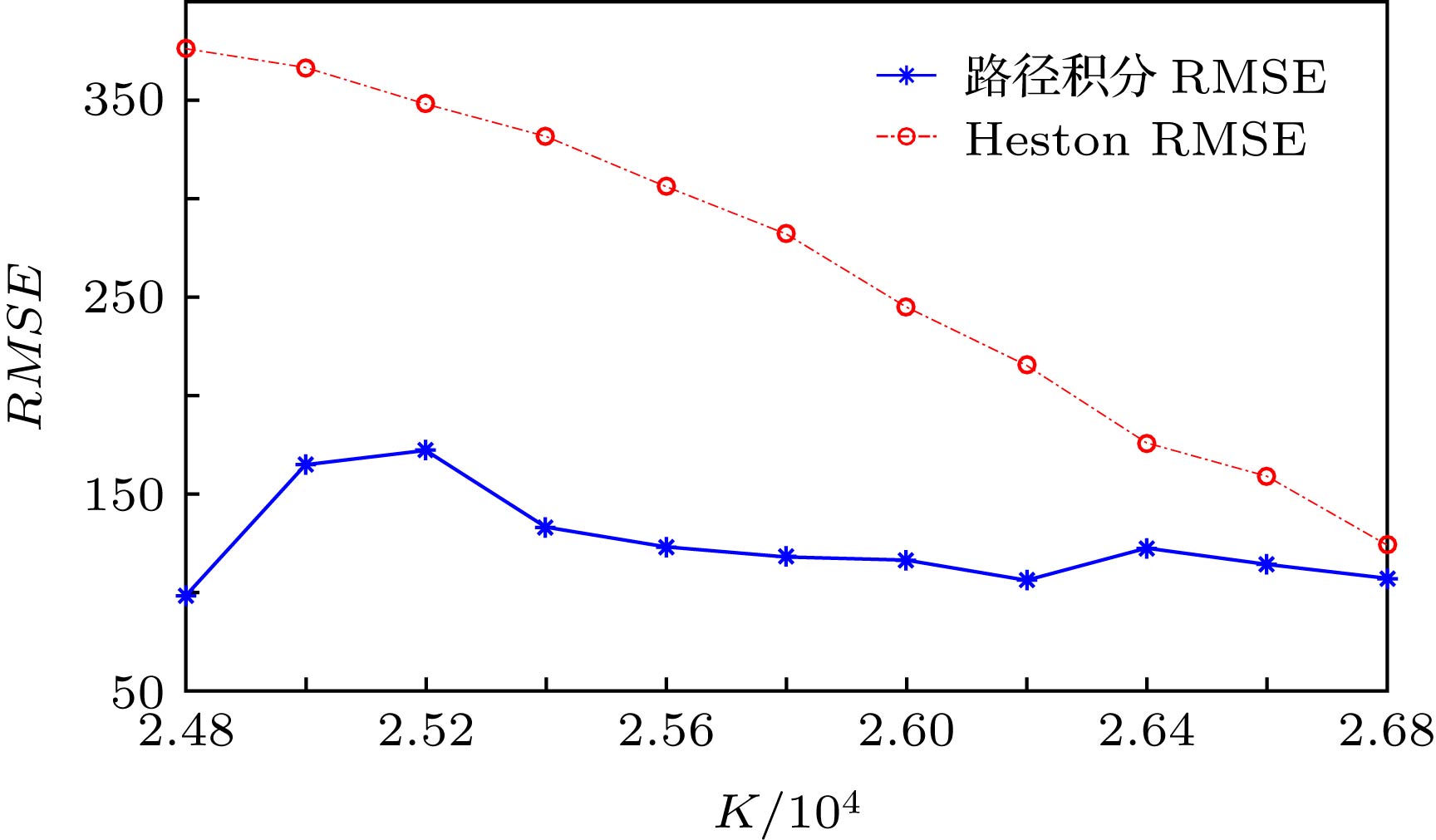

表 2 K = 25800下两种模型不同到期日下的评价指标值

Table 2. K = 25800, the evaluation index values of the two models under different maturity dates.

到期日 RMSE Theil不等系数 费曼路径积分 Heston 费曼路径积分 Heston 2019年2月 113.1631 269.8452 0.0429 0.1138 2019年3月 118.0685 282.0939 0.0401 0.1037 2019年6月 94.7388 87.9670 0.0275 0.0259 2019年9月 88.4829 230.9288 0.0230 0.0584

下载: 导出CSV

-

[1] Pan J 2002 J. Financ. Ecno. 63 3

Google Scholar

[2] Eraker B, Johannes M, Polson N 2003 J. Financ. 58 1269

Google Scholar

[3] Broadie M, Chernov M, Johannes M 2007 J. Financ. 62 1453

Google Scholar

[4] 杨智元, 陈浪南 2001 经济研究 47 61

Yang Z Y, Chen L N 2001 J. Econ. Res. 47 61

[5] Duan J C, Zhang H 2001 J. Bank Financ. 25 1989

Google Scholar

[6] 魏洁, 韩立岩 2016 数理统计与管理 33 550

Wei J, Han L Y 2016 J. Appl. Stat. Manag. 33 550

[7] 杨兴林, 王鹏 2018 数理统计与管理 37 162

Yang X L, Wang P 2018 J. Appl. Stat. Manag. 37 162

[8] Bailey W, Stulz R M 1989 J. Financ. Quant. Anal. 24 1

Google Scholar

[9] 谭朵朵 2008 统计与信息论坛 23 40

Google Scholar

Tan D D 2008 Stat. Inform. Forum 23 40

Google Scholar

[10] 韩立岩, 叶浩, 李伟 2012 中国管理科学 20 23

Han L Y, Ye H, Li W 2012 Chinese J. Manag. Sci. 20 23

[11] 樊鹏英, 陈敏 2014 价格理论与实践 34 96

Fan P Y, Chen M 2014 Price Theor. Pract. 34 96

[12] [13] Baaquie B E 1997 J. Phys. I 7 1733

[14] Linetsky V 1998 Computaitonal Ecomomics 11 129

Google Scholar

[15] Baaquie B E, Coriano C, Srikant M 2002 Quant. Financ. 15 333

[16] Baaquie B E 2004 Quantum Finance (Singapore: Cambridge University Press) pp78–116

[17] Baaquie B E, Corianò C, Srikant M 2004 Phys. A 334 531

Google Scholar

[18] Baaquie B E 2013 Comput. Math. Appl. 65 1665

Google Scholar

[19] Rosa-Clot M, Taddei S 1999 Quant. Financ. 5 123

[20] Kakushadze Z 2015 Quant. Financ. 15 1759

Google Scholar

[21] Issaka A, Sengupta I 2017 J. Appl. Math. Comput. 54 159

Google Scholar

[22] Ma C, Ma Q, Yao H, Hou T 2018 Phys. A 494 87

Google Scholar

[23] Paolinelli G, Arioli G 2018 Phys. A 517 499

[24] 陈泽乾 2003 数学物理学报 23 115

Google Scholar

Chen Z Q 2003 Acta Math. Sci. 23 115

Google Scholar

[25] 陈黎明, 邱菀华 2007 中国管理科学 15 12

Google Scholar

Chen L M, Qiu W H 2007 Chinese J. Manag. Sci. 15 12

Google Scholar

[26] 王鹏, 魏宇 2014 管理科学学报 17 40

Wang P, Wei Y 2014 J. Manag. Sci. China 17 40

[27] Heston S L 1993 Rev. Financ. Stud. 6 327

Google Scholar

[28] Scott L O 1987 J. Financ. Quant. Anal. 22 419

Google Scholar

[29] Merville L J, Pieptea D R 1989 J. Financ. Econ. 24 193

Google Scholar

[30] Stein E M, Stein J C 1991 Rev. Financ. Stud. 4 727

Google Scholar

[31] Cox J, Ingersoll J, Ross S 1985 Econometrica 53 385

Google Scholar

[32] 施里夫 S 著(陈启宏, 陈迪华 译) 2008 金融随机分析(上海: 上海财经大学出版社)第192—193页

Shreve S (translated by Chen Q H, Chen D H) 2008 Stochastic Calculus for Finance (Vol. 2) (Shanghai: Shanghai University of Finance and Economics Press) pp192–193 (in Chinese)

[33] 杨爱军, 蒋学军, 林金官, 刘晓星 2016 数理统计与管理 35 817

Google Scholar

Yang A J, Jiang X J, Lin J G, Liu X X 2016 J. Appl. Stat. Manag. 35 817

Google Scholar

[34] Durrett R 2016 Essentials of Stochastic Processes (New York: Springer) pp223–250

[35] Baaquie B E, Kwek L C, Srikant M 2000 arXiv: 0008327v1 [cond-mat] https://arxiv.org/abs/cond-mat/0008327 [2019-5-1]

下载:

下载:

计量

- 文章访问数: 11583

- PDF下载量: 103

- 被引次数: 0